Στην υγειά του Σπύρου Λάτση!

Ποιοι και πώς έθαψαν το σκάνδαλο με το ξέπλυμα μαύρου χρήματος πελατών της EFG και πώς ο Σπύρος Λάτσης κατάφερε να διασώσει την τράπεζά του με λεφτά του ελληνικού λαού!

Τελικά σε αυτή τη χώρα δεν πρόκειται να αλλάξει απολύτως τίποτα, αφού το σύστημα εξουσίας συνεχίζει να ευνοεί τους ίδιους επιχειρηματίες που επί σειρά δεκαετιών έβγαλαν ένα… σκασμό λεφτά στις πλάτες του ελληνικού λαού.

Την ώρα που εκατοντάδες χιλιάδες μικρομεσαίες επιχειρήσεων βάζουν λουκέτο λόγω οικονομικής ασφυξίας, με την πραγματική ανεργία να ξεπερνά το 30% και εκατομμύρια συνταξιούχων να κινδυνεύουν να χάσουν τις συντάξεις τους, το ελληνικό κράτος συνεχίζει να βάζει το κεφάλι του στον… ντορβά για «εκλεκτούς» επιχειρηματίες, οι οποίοι «σαρώνουν» όλες τις δουλειές, από τα πετρέλαια μέχρι το real estate.

Η κυβέρνηση των «αδιάφθορων» αριστερο-δεξιών που δήθεν ψάχνει ισοδύναμα για να μην κόψει τις κύριες συντάξεις των Ελλήνων, μπαίνει ως εγγυήτρια για να μην χρειάζεται φίλοι επιχειρηματίες (ακόμα και αν αυτοί, τύποις, έχουν αποχωρήσει από το μετοχικό κεφάλαιο) να βάζουν το χέρι στην τσέπη κατά τη διάσωση των τραπεζών τους.

«Σοσια-ληστικά» πράγματα δηλαδή!

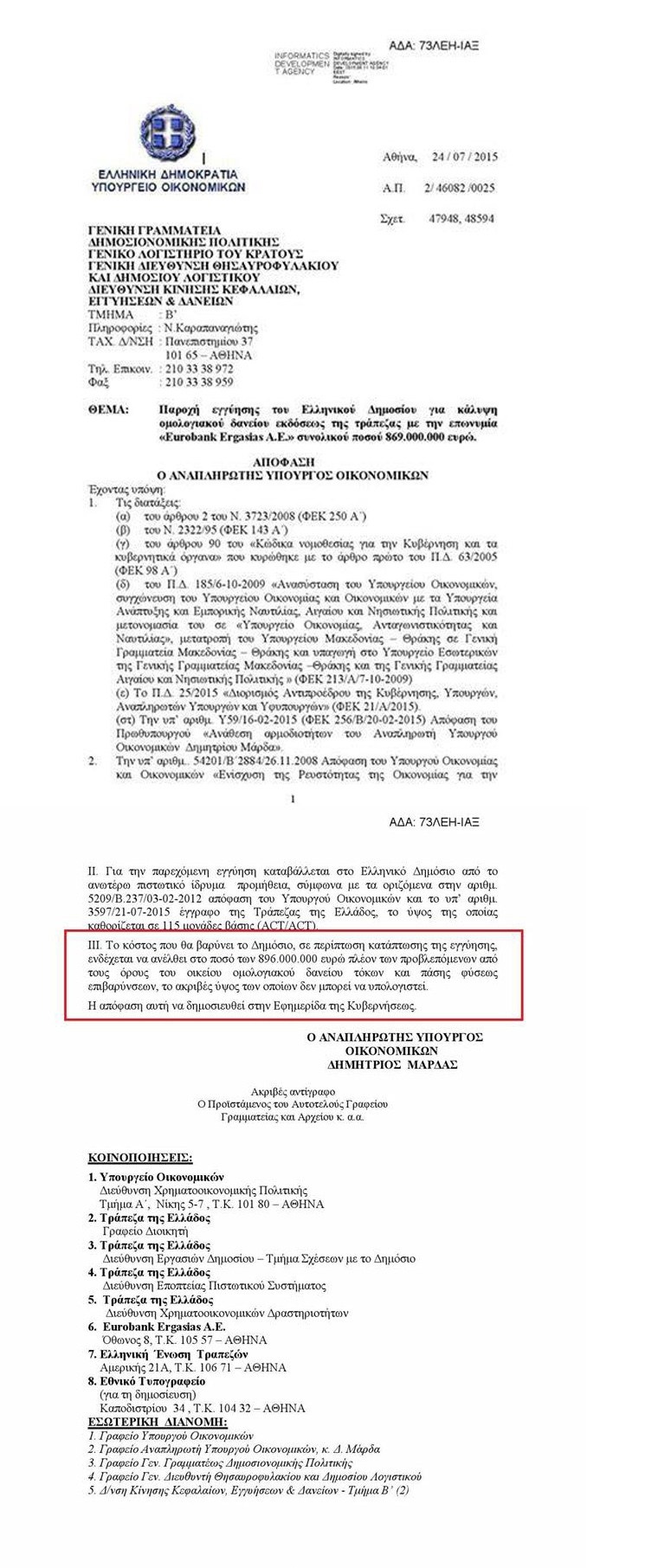

Μόλις πριν από λίγους μήνες και ενώ η χώρα βρίσκεται στην κυριολεξία στο γκρεμό, οι «αδιάφθοροι» Τσίπρας και Καμμένος αποφάσισαν με συνοπτικές διαδικασίες να μπει το ελληνικό δημόσιο ως εγγυητής για κάλυψη ομολογιακού δανείου της Eurobank, ύψους 900 εκατ. ευρώ!

Η υπόθεση είναι βεβαίως γνωστή στην πολιτική και στη δημοσιογραφική πιάτσα. Πλην όμως κανένα ΜΜΕ δεν τόλμησε να αναδείξει έστω και το παραμικρό.

Και όλα τα παραπάνω βεβαίως λαμβάνουν χώρα επί κυβερνήσεως «πρώτης φοράς Αριστερά».

Αξίζει να σημειωθεί πως στην απόφαση ρητώς αναφέρεται ότι σε οποιαδήποτε κατάπτωση της εγγύησης, αυτή οφείλει να καταβληθεί από το Ελληνικό Δημόσιο, δηλαδή από τους έλληνες φορολογουμένους!

Η Σχετική Απόφαση έχει ημερομηνία 24-07-2015 και φέρει την υπογραφή του τότε Αναπλ. Υπουργού Οικονομικών, Δημήτρη Μάρδα.

Δείτε την απόφαση:

Κι όλα αυτά για τον «εκλεκτό» μεγιστάνα Σπύρο Λάτση. Ναι, τον κύριο που έχτισε το Mall χωρίς άδειες, που θα πάρει το Ελληνικό έναντι πινακίου φακής, που ελέγχει τις τιμές του πετρελαίου στην Ελλάδα και που έσωσε και την τράπεζά του χωρίς να βάλει δεκάρα τσακιστή.

Ποια τράπεζα;

Αυτή που βρέθηκε στο στόχαστρο των Βρετανικών αρχών πριν από λίγα χρόνια για ξέπλυμα μαύρου χρήματος!!!

Ούτε αυτό το γνωρίζετε;

Στ’ αλήθεια κανείς δεν γνωρίζει τι απέγινε η εμπλοκή 94 πολιτικών προσώπων – πελατών της EFG που μπήκαν στο στόχαστρο για πιθανό ξέπλυμα μαύρου χρήματος από Βρετανική αρχή;

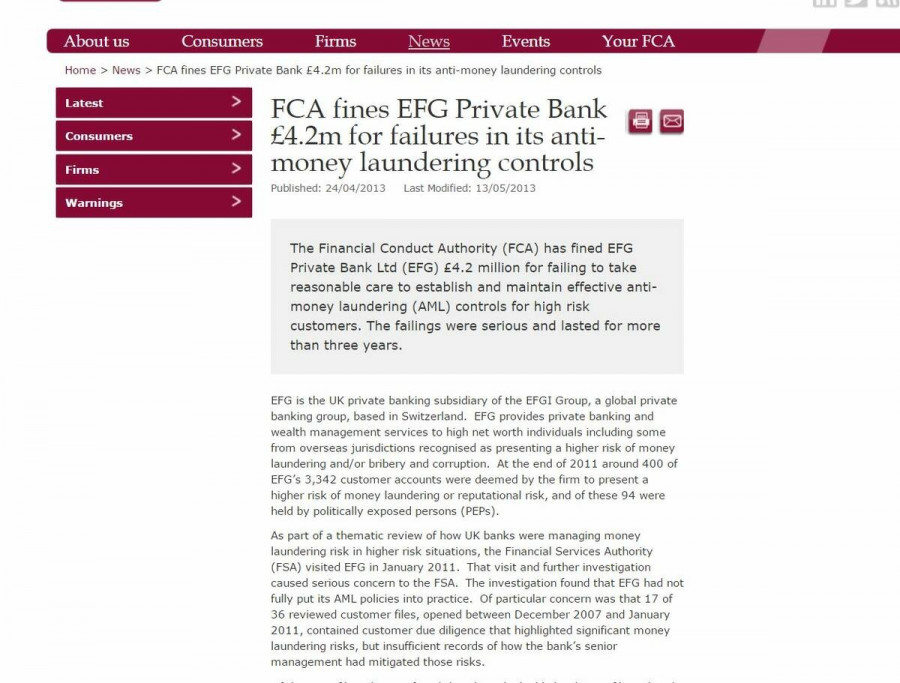

Κανείς δεν γνωρίζει για τους ελέγχους που έκανε το 2013 ο Βρετανικός FCA (Finance Contact Authority) και κατά τον οποίο βρέθηκαν 17 μυστήριοι φάκελοι από το Δεκέμβρη του 2007 έως τον Γενάρη του 2011 από τους 36 που ελέχθηκαν δειγματοληπτικά;

Κανείς δεν άκουσε τίποτα για το πρόστιμο 4,2 εκατομμυρίων στερλινών για την EFG και την εταιρεία CMA η οποία εξαγοράστηκε από τον Σπύρο Λάτση;

Προφανώς τα πρόστιμα πληρώθηκαν και η υπόθεση «έκλεισε», όπως συνηθίζεται σε αυτές τις περιπτώσεις ξεπλύματος μαύρου χρήματος.

Άλλως πώς μπορεί να εξηγηθεί τέτοια σιωπή;

Ο έλεγχος πάντως του FSA έδειξε σημεία και τέρατα, όπως θα δείτε και από τα ντοκουμέντα που ξεσκεπάζει το Newsbomb.gr

Από τους 3.342 πελάτες, οι 400 χαρακτηρίζονται «υψηλού ρίσκου» για ξέπλυμα μαύρου χρήματος, εκ των οποίων 94 είναι πολιτικά πρόσωπα ή πρόσωπα που σχετίζονται με την πολιτική (συγγενείς κ.λπ)!!

Υπάρχουν περιπτώσεις ακόμα και «νονού» του οργανωμένου εγκλήματος που κατηγορείται και για δολοφονίες του οποίου ο γιος έγινε «πελάτης» της EFG χωρίς να γίνουν οι προβλεπόμενοι έλεγχοι.

Τα ευρήματα αφορούσαν μόνο την Βρετανία. Υπάρχει ακόμα και το Λουξεμβούργο, η χώρα – σκάνδαλο στην οποία η EFG έχει τεράστια δραστηριότητα. Κάποιοι μιλούν και για κινήσεις στην δευτερογενή αγορά.

Βεβαίως πρέπει να συμπληρώσουμε ότι κανένας αρμόδιος ελληνικός κρατικός μηχανισμός δεν ζήτησε να παραλάβει τον εν λόγω έλεγχο του Βρετανικού οργανισμού, όπως κανείς δεν ενδιαφέρθηκε ποτέ για τις λίστες Λαγκάρντ, Φαλτσιανί κ.λπ.

Δείτε την ανακοίνωση από την επίσημη ιστοσελίδα του Αγγλικού οργανισμού και θα καταλάβετε για τι σκάνδαλο μιλάμε!!!

FCA fines EFG Private Bank £4.2m for failures in its anti-money laundering controls

Published: Yesterday

The Financial Conduct Authority (FCA) has fined EFG Private Bank Ltd (EFG) £4.2 million for failing to take reasonable care to establish and maintain effective anti-money laundering (AML) controls for high risk customers. The failings were serious and lasted for more than three years.

EFG is the UK private banking subsidiary of the EFGI Group, a global private banking group, based in Switzerland. EFG provides private banking and wealth management services to high net worth individuals including some from overseas jurisdictions recognised as presenting a higher risk of money laundering and/or bribery and corruption. At the end of 2011 around 400 of EFG’s 3,342 customer accounts were deemed by the firm to present a higher risk of money laundering or reputational risk, and of these 94 were held by politically exposed persons (PEPs).

As part of a thematic review of how UK banks were managing money laundering risk in higher risk situations, the Financial Services Authority (FSA) visited EFG in January 2011. That visit and further investigation caused serious concern to the FSA. The investigation found that EFG had not fully put its AML policies into practice. Of particular concern was that 17 of 36 reviewed customer files, opened between December 2007 and January 2011, contained customer due diligence that highlighted significant money laundering risks, but insufficient records of how the bank’s senior management had mitigated those risks.

Of these 17 files, the FSA found that the risks highlighted in 13 files related to allegations of criminal activity or that the customer had been charged with criminal offences including corruption and money laundering.

For example in one account, EFG’s due diligence highlighted that a prospective client had acquired their wealth through their father, about whom there were allegations of links with organised crime, money-laundering and murder. However there was insufficient information on file to explain how the bank concluded that this risk was acceptable or how it was mitigating the risks.

EFG also failed to appropriately monitor its higher risk accounts. Of the 99 PEP and other high risk customer files reviewed by the FSA, 83 raised serious concerns about EFG’s monitoring of the relationship.

As a result of these failures, EFG breached FSA Principle 3, requiring it to take reasonable care to organise and control its affairs responsibly and effectively.

Tracey McDermott, head of enforcement and financial crime, said:

«One of the FCA’s objectives is to protect and enhance the integrity of the UK financial system. This includes ensuring money in the UK system is clean.

«Banks are the first line of defence to make sure that proceeds of crime do not find their way into the UK. In this case while EFG’s policies looked good on paper, in practice it manifestly failed to ensure that it was addressing its AML risks. Its poor implementation of its agreed policies risked the bank handling the proceeds of crime. These failures merited a strong penalty from the FCA.

«Firms that accept business from high risk customers must have systems, controls and practices to manage that risk. The FCA will continue to focus on high risk customers and business.»

EFG settled at an early stage of the investigation and qualified for a 30% discount on its fine. Without the discount the fine would have been £6 million.

Notes for editors

The Final Notice for EFG Private Bank Ltd.

On 22 June 2011, the FSA published its findings from a thematic review, which focused on how banks manage money laundering risk in higher risk situations. The FSA published a Policy Statement PS11/15 Financial crime: a guide for firms on 9 December 2011. This contains guidance on steps firms can take to reduce their financial crime risk, including in their dealings with high risk and PEP customers.

EFG breached Principle 3 of the FCA’s Principles for Businesses. Principle 3 is set out in the FCA Handbook and states: a firm must take reasonable care to organise and control its affairs responsibly and effectively, with adequate risk management systems.

The FSA fined Coutts and Habib Bank for similar AML failings.

On the 1 April 2013 the Financial Conduct Authority (FCA) became responsible for the conduct supervision of all regulated financial firms and the prudential supervision of those not supervised by the Prudential Regulation Authority (PRA).

The FCA has an overarching strategic objective of ensuring the relevant markets function well. To support this it has three operational objectives: to secure an appropriate degree of protection for consumers; to protect and enhance the integrity of the UK financial system; and to promote effective competition in the interests of consumers

You can find more information about the FCA, as well as how it is different to the PRA.